Credit: Schroders

By Ovidiu Patrascu, Schroders

A growing proportion of companies are led by their founders; 7% of globally listed companies with market capitalisations above $500 million are run by their founders (source: Bloomberg).

Among initial public offerings (IPO) the tendency is more common; 30% of the companies listed globally over the last five years are led by their founders. In those cases where track records are limited, the role and effectiveness of business leaders is often judged by intuition more than analysis.

We expect the issue to become increasingly important. Companies can scale quicker than ever in capital-light, global industries. With venture capital war chests still strong, public market capital is little impediment to scaling a good idea quickly.

In addition, the widespread use of the internet allows companies to quickly tap global customers, employees and suppliers, bypassing the traditional expansion from local to national to international. As a result, it is increasingly likely that the founder will still be in charge by the time IPO scale is reached.

Our approach

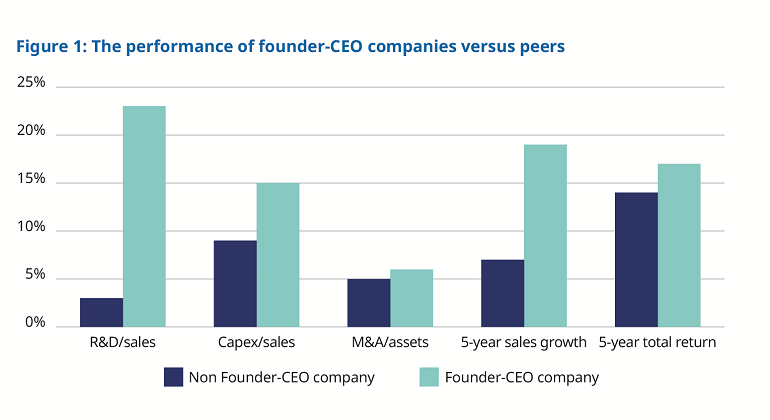

We set out to explore whether companies led by their founders tend to take a more long-term approach in capital allocation, enjoy superior profitability or perform better than peers. We examined 3,600 non-financial companies with market capitalisations over $500 million. Approximately 70% of founder-led companies are listed in the US, followed by China (8%), Japan (7%) and Europe (6%), and the majority operate in the technology, pharmaceuticals and retail sectors (source Bloomberg 31 Dec 2016).

Founder-CEO companies outperform

Our research demonstrates that in general:

Founder-CEO companies invest more aggressively than their peers in research and development (R&D), capital expenditure (capex), and mergers and acquisitions (M&A)

They grow revenues at a faster pace

Their share prices have outperformed peers over the 5-year period to December 2016

Sector-specific differences

However, our findings become more nuanced when looking at specific sectors in more detail.

Founder-CEO companies operating in innovation intensive sectors such as internet, software, biotechnology and pharmaceuticals tend to invest more in R&D, capex and M&A than their peers. This often leads to better revenue growth, but not to share price outperformance.

In more capital intensive industries such as hardware and semiconductors, founder-CEO companies tend to allocate capital more conservatively, and their share prices have generally outperformed their peers.

In some mature but profitable industries, such as electronic & electrical equipment, founder-CEO companies allocate more capital but at relatively high levels of profitability. This leads to strong compounding power and share price outperformance.

Enabling better research focus

Founder-CEOs are often found in the most exciting areas of the market. By objectively examining their influence on capital allocation and investment performance, our investment teams are better able to focus their research efforts into specific sectors where founder-CEO companies are more likely to outperform their peers.

The full article is available here.

Schroders is a world-class asset manager operating from 32 countries across Europe, the Americas, Asia, the Middle East and Africa. As of December 31st 2018, Schroders is responsible for £421.4 billion (€469.5 billion/$536.7 billion) of assets for clients and 5,000 people across six continents focused on delivering sustainable returns.